Retail Trade—Revenue Growth and the Resurgence of the National Brands Trend

Experts at UTG company continue to analyze the state of retail real estate in Ukraine. According to the “Strategic Consulting Department,” the positive trend of retail revenue growth continues in Ukraine. Based on the results for the first four months of 2026 (January-April), retail trade grew by +18.89% in local currency to 931.12 billion UAH and by +12.53% in dollar terms. One of the main reasons for the growth in recent years is the resurgence of the trend towards developing national brands.

Retail and Brands

Retail sales by Ukrainian manufacturers are increasing amid a rapid rise in loyalty to Ukrainian fashion among both the local population and visitors to the country. Seizing the opportunity, these brands have launched aggressive expansion efforts, are gaining momentum, and are moving from online platforms to brick-and-mortar retail by opening stores: rikky hype, Katy Soho, Cher 17, Solmar, PetHouse, Gorgany, and others. According to forecasts by UTG analysts and market experts, the future growth potential for Ukrainian brands is quite high.

In addition, once the war ends, increased loyalty toward Ukraine is expected, along with the start and resumption of negotiations with a wide range of international brands: “Starbucks,” “Uniqlo,” “Pepco”, “Peek & Cloppenburg”, “Kiabi”, “Abercrombie & Fitch”, “Hollister”, “Profuomo”, “Daily Paper”, “Suitsupply”, and “Mason Garments” – as well as a real opportunity for new brands that were previously unrepresented or had ignored the country to enter the Ukrainian market.

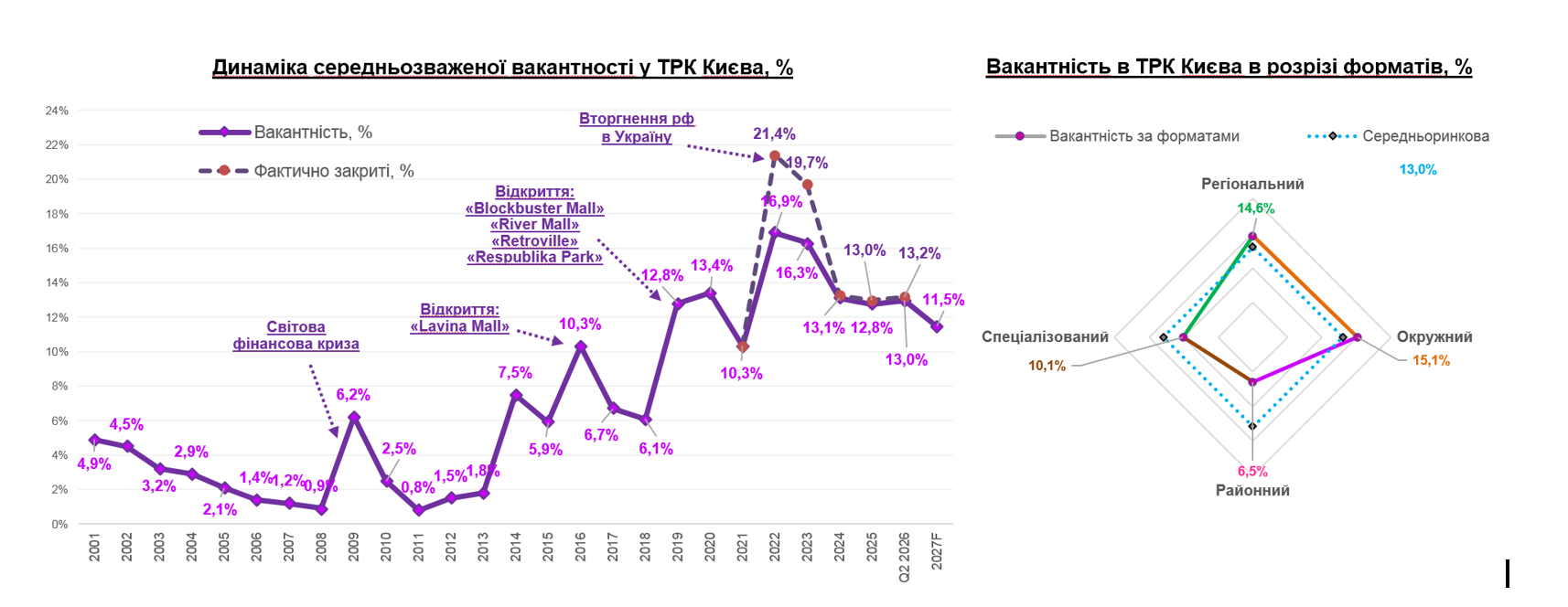

Retail Space

Although the active retail development of the pre-war years has slowed, it continues, as does the further saturation of the market with retail space. As a result, the dispersion of foot traffic among properties is deepening, and vacancy rates are rising. Furthermore, the challenges faced by entertainment operators (fitness centers, movie theaters, entertainment centers, bowling alleys, and restaurants) during the COVID-19 pandemic have been exacerbated by the war – including closures during air raid alerts, curfews, and other restrictions.

Against this backdrop, vacancy rates are gradually evening out across different shopping center formats. According to the analysis, the vacancy rate in regional shopping centers stands at 14.6%, in district shopping centers at 15.1%, and in specialized SCs at 10.1%. As before, the lowest vacancy rate – 6.5% – is characteristic of neighborhood SCs located near areas of high population density.

Specifically, the main vacant spaces are concentrated in four properties: “Blockbuster Mall,” “Marmalad,” “Promenada Center,” and “Atmosfera.” However, the exit of Russian retailers from the market, the closure of international chains (such as IKEA), the lack of alternative department stores, and a pause in the entry of new foreign brands are limiting the potential for reducing vacant space. Furthermore, the prospect of opening new large-scale SCs amid a limited selection of retailers makes it even more difficult to attract tenants and increases vacancy rates. Another significant factor is the shift in developers’ interests due to the war – they are now considering other regions, new segments, and alternative industries.

All of this heightens the need to restructure shopping centers and carry out post-war reconceptualization in a number of commercial properties, including under extreme scenarios.

Rental Rates

Rising operating costs and the need to cut expenses across the board – including advertising, marketing, utilities, electricity, water, heating, air conditioning, and generator maintenance – are limiting the potential for rental rate increases. Growth prospects are also negatively impacted by the decline in gross rental rates per square meter and retailers’ profit margins in recent years – driven by a gradual increase in competitive offerings, a decrease in average daily foot traffic, and lower sales at individual stores.

Landlords themselves are also keeping rental rates in check by implementing policies designed to minimize retailers’ risks and shift those risks onto the developer – by setting a minimum payment, linking rent to a percentage of gross sales, to the occupancy rate of the retail property, or to actual foot traffic figures.