The vacancy rate of commercial real estate in Kyiv may reach 17% by the end of 2024

At the current level of income and expenditure of the population, the vacancy rate of SECs in Kyiv may reach 17% by the end of 2024, the head of the Strategic Consulting Department of UTG Kostyantyn Oliynyk told the Interfax-Ukraine agency.

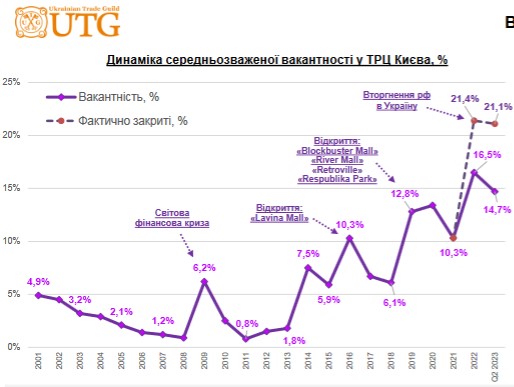

According to UTG research, the vacancy rate of the capital’s shopping malls decreased from 16.5% at the end of 2022 to 14.7% at the end of the second half of 2023. Taking into account stores of international brands that are temporarily closed, 21.1% of the space is vacant (it was 21.4% at the end of 2022). Before the war, 10.3% of the area was vacant.

“Taking into account the current level of income of the population, solvent demand is able to ensure the successful operation of 2 million 313 thousand square meters of retail space. While as of August 2023, 2 million 457 thousand square meters are already functioning in Kyiv. Commissioning by of declared projects with a total area of more than 250,000 square meters by the end of 2024 will bring the surplus of retail space even closer and stimulate the gradual redistribution of consumer flows between objects. All this will lead to an increase in vacancy to 17% and a downward correction of rental rates.” – Oliynyk said.

At the same time, in 2023-2024, shopping centers White Lines (28 thousand square meters), New Ray (34.5 thousand square meters), April Mall (36.5 thousand square meters), BalticSky (20 thousand square meters), Ocean Mall (GLA – 110 thousand square meters), Lukiyanivka (47,052 thousand square meters) and other objects.

Oliynyk emphasized that in a situation of market saturation, any opening of a new large-format shopping center against the background of a limited assortment of active retailers affects the average market vacancy rate and makes it difficult to attract tenants.

According to him, management companies have already faced many difficulties: the total exit of Russian chains, the lack of a sufficient number of alternative international department stores on the vacated areas, the closure of large-format international operators before the end of hostilities (Inditex, H&M, IKEA, M&S, GAP), uncertainty in the restoration of full-fledged work of entertainment operators (fitness centers, cinemas, children’s entertainment centers, bowling alleys, food establishments).

As UTG analysts predict, there is a high probability of serious difficulties in filling large-format facilities in the medium term (lack of anchors, department stores). Such trends lead to forced modernization, redevelopment and reconceptualization of existing shopping centers.

He recalled that before the war, a number of developers started or carried out complex modernization of their projects (Caravan, TsUM, Metrograd, Metropolis, Kvadrat Lukyanivka, Cosmo Multimall, Gorodok Gallery, Magellan, Globus, Marmalade, Dream Town, Silver Breeze, InSilver), a number of owners planned large-scale changes in the near future.

For now, this trend will continue, “including extreme solutions,” Oliynyk stressed.

The UTG company was established in 2001. Developed more than 1,300 concepts of real estate objects. During the years of work, 4.7 million sq.m were leased with the participation of the company of commercial space in Ukraine.