Financial instruments and mortgage lending for housing

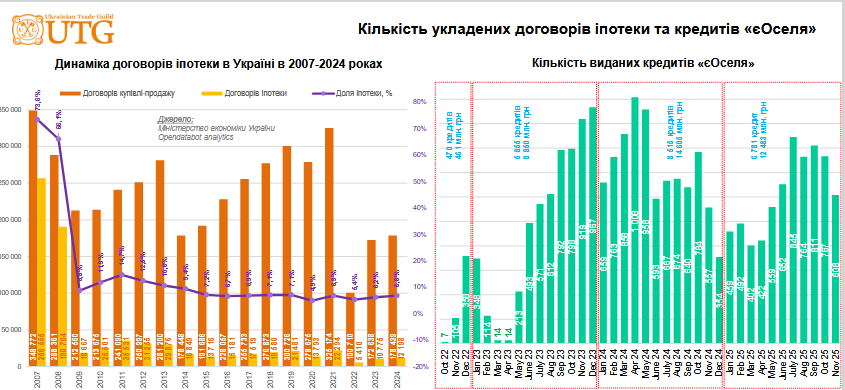

The housing financing market in Ukraine has gone from almost complete standstill in 2022 to revival, although the mortgage market in the country has been extremely poorly developed in recent years. After the peak of 2007–2008 (when the number of mortgage contracts reached 190–348 thousand per year), a long period of stagnation set in. In 2021, before the full-scale war, only 22,294 mortgage contracts were concluded, with a total number of purchase and sale transactions of 325,174 (the share of mortgages is 6.8%). In 2022, the market collapsed to a minimum of 5,410 mortgage contracts. However, the launch of the state preferential lending program “eOselya” became a turning point. In 2024, the number of mortgage agreements increased to 10,775, which is 6.0% of the total number of purchase and sale agreements (178,439). And, according to the Ministry of Economy of Ukraine, as of December 2025, Ukrainians had taken out a total of 21,621 e-Housing loans worth UAH 36.39 billion. The average loan amount is UAH 1,683,502 (approximately $39,363).

The e-Housing program started in October 2022 with 17 loans, but in December of the same year the number increased to 358. The real take-off occurred in May 2023 (2,113 loans), after which the indicators stabilized within 600–1,000 loans per month.

However, the program has a clearly defined social focus. The main categories of recipients of preferential mortgages (at 3–7% per annum for a period of up to 20 years) are military personnel and representatives of the security sector – 28.9% or security guards – 21.8%. The share of others is 26.6%, including: teachers – 8.9%, medical workers – 8.4%, employees of the State Emergency Service – 5.5%, scientists – 2.0% and IDPs and veterans – about 1.8%.

The greatest demand for the “e-Housing” program is concentrated in the capital region: 5,591 loans were issued in the Kyiv region, 4,324 in Kyiv. This confirms the concentration of solvent demand and the activity of developers in this area.

As for the structure of “e-Housing” housing, there is a dominance of secondary housing – 60.6% (12,149 loans) falls on it. The share of the primary market (objects under construction) is only 9.0% (1,801 loans), and ready-made housing directly from the developer occupies 30.5% (6,111 loans). The state is trying to gradually reduce the share of the secondary market in the program in order to stimulate new construction. 98 developers have already joined the program.

The main operators of the program are state-owned banks: Oschadbank occupies 42% of the market, Privatbank – 30.1%, Ukrgasbank – 23.9%. Private banks (Sky Bank, Sense Bank, Globus and others) have a total share of less than 4%. This indicates a high dependence of the mortgage market on state liquidity and political will.

But, despite the success of “eOselya”, the general underdevelopment of the mortgage market remains a problem. The main obstacles are the shortage of solvent borrowers, strict lending conditions (especially for the civilian population) and a low level of protection of creditors’ rights. Therefore, for real buyers, the tool of deferral from the developer remains extremely relevant, which is often more flexible, although more expensive in the short term.

According to the forecasts of UTG company experts, in 2026 and 2027 the program with “e-Housing” will become the main engine of the market. At the same time, there will be a change in focus on the primary market. State policy will be aimed at increasing the share of lending to objects under construction. This is necessary to stimulate the economy and create new jobs. It is expected that the share of “primary” in “e-Housing” will increase to 45-50% in 2026. It is also possible to further expand the list of categories of citizens who can apply for a 7% rate, which could increase the number of potential borrowers by 15-20%. In 2026-2027, commercial banks are expected to be more actively involved in the program, which could slightly reduce the burden on the state budget.

The main risk for housing lending remains the limited financial resources of the state. If the volume of e-Housing financing decreases, the housing market may again fall into stagnation, as alternative mortgage products from banks with market rates remain inaccessible to most Ukrainians.