Dynamics of housing commissioning volumes in Ukraine: from record to adaptationsing

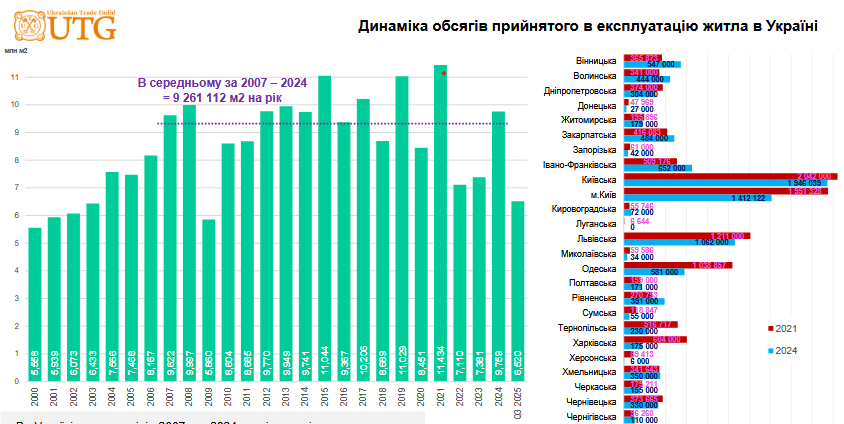

UTG company analysts continue to study the state of the Ukrainian market. According to the State Statistics Committee of Ukraine, the full-scale invasion in February 2022 radically changed the landscape of housing construction. In 2022, the volume of housing commissioning decreased to 7.110 million sq. m, which was the expected result of the suspension of most construction sites in the first and second quarters. However, already in 2023, there was a slight recovery to 7.381 million sq. m, and the results of 2024 were a real surprise for market analysts: the volume of housing commissioned amounted to 9.759 million sq. m. And according to the results of the three quarters of 2025, 6.52 million sq. m have already been commissioned, which indicates that the pace of construction work is maintained.

Such dynamics are explained by several strategic factors. Firstly, developers made every effort to complete projects with a high degree of readiness in order to fulfill their obligations to investors and avoid bankruptcy. Secondly, there was a significant shift of construction activity to safer regions in the western part of the country. Thus, geographical analysis demonstrates a striking contrast between regions. Military operations contributed to a complete halt in work in some regions, while others became “rear hubs” for developers. For example, the Kyiv region demonstrated impressive growth, becoming the undisputed leader in terms of housing commissioning in 2025. This is explained both by the relocation of business and the high demand for housing in the suburban area of the capital, which is considered relatively safer and more affordable. At the same time, volumes in Kharkiv region fell more than threefold, and in Odessa – almost twofold, which is directly related to the intensity of shelling and security risks for investors. In western regions, such as Ivano-Frankivsk and Vinnytsia regions, there is a steady positive trend, driven by the influx of internally displaced persons (IDPs) and capital from eastern regions.

But the pace of construction work may decrease significantly as early as 2026. One of the main problems at construction sites remains the lack of working personnel. Mobilization and outflow of personnel abroad have led to a shortage of qualified engineers and workers, which is a critical factor for the future pace of recovery.