Housing stock and construction costs

Based on the data for the three quarters of 2025 and the current dynamics, it is possible to predict the preservation of the pace of housing commissioning. It is expected that by the end of 2025 the total volume will be about 8.5–9.0 million sq. m. And in 2026 the volumes may stabilize at the level of 9.0–9.5 million sq. m, provided that construction continues to be concentrated in safe regions. Based on this, the Western regions of Ukraine will continue to increase their share in the national construction volume. Although the Kyiv region may retain its leadership, the growth rates in the Ivano-Frankivsk and Vinnytsia regions may accelerate.

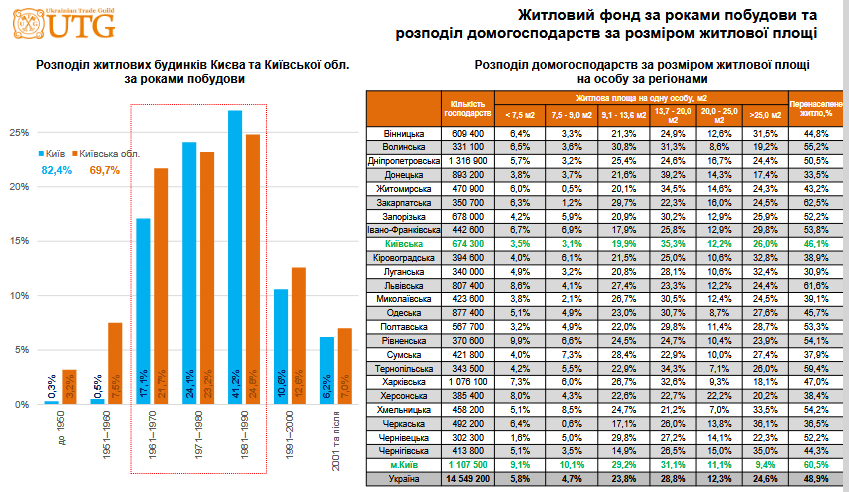

Against the background of problems with the outdated stock, the problems of houses built in the 1960s–1980s will intensify. Therefore, an increase in demand for new housing is expected, especially from the owners of apartments in outdated panel houses. The situation in Kyiv and Kyiv region is most representative for understanding the challenges facing the market. The capital’s housing stock consists of approximately 10,500 houses, but its structure is extremely uneven. 2,500 houses were built before 1941, and the vast majority of housing — 82.4% — was put into operation in 1960–1990. This is mainly panel construction, the standard operating life of which is 50 years. This fact means that a significant part of the capital’s housing stock has already exhausted its technical resource or is approaching this limit.

This creates a huge deferred demand for new housing and the need for comprehensive renovation of outdated neighborhoods, which will stimulate the primary real estate market. But the lack of labor will remain the main challenge for developers and the development of primary real estate in 2026. This may lead to the gradual introduction of more automated construction methods and prefabrication.

Also, the cost of housing construction will become a key indicator that determines the pricing policy of developers and the availability of real estate for the end consumer. For example, the Ministry of Community and Territorial Development of Ukraine, by order No. 60 dated 01-15-2026, approved the forecast average annual indicators of the indirect cost of housing construction by region, calculated as of 01/01/2026. These indicators are based on the cost of construction of 1 total area of the house, including VAT, but they do not include a number of critically important costs and reflect only the “net” cost of construction. For a real development project, it is necessary to take into account additional loads, such as: the cost of attracting a land plot (an additional 8–15% to the cost), advertising, marketing and general promotion of the complex, the cost of attracting financial resources and servicing loans, the costs of organizing the work of sales departments, other operational and administrative costs of the developer. This means that the market price of housing will always be significantly higher than the indirect cost indicators due to the need to cover these items and make a profit.

Analysis of cost dynamics showed steady growth across the country. Thus, the average price in Ukraine from January 2021 to January 2026 almost doubled: from UAH 13,231 to UAH 25,739 per sq. m. At the same time, the highest construction cost is traditionally observed in Kyiv, where as of January 2026 it reached UAH 30,081 per sq. m. This is explained by the complexity of engineering solutions, the higher cost of logistics within the metropolis and higher salary expectations of personnel. The lowest indicators were recorded in Kirovohrad (UAH 21,875 per sq. m) and Zakarpattia (UAH 22,343 per sq. m) regions. However, despite the construction boom in Zakarpattia, the cost price there remains relatively competitive due to the availability of certain types of raw materials and the peculiarities of the local labor market.

Factors of the increase in value, if we consider that the main acceleration of the increase in value occurred between 22 and 23 years, when the average indicator in Ukraine jumped from 16,003 UAH per sq. m to 20,259 UAH – this was a direct consequence of the devaluation of the national currency, the increase in prices for energy and fuel, as well as the destruction of large metallurgical and cement plants. In subsequent years (2024–2026), growth stabilized at about 8–12% per year.

There are also additional influencing factors: the increase in the cost of building materials, which is interconnected with the import dependence of certain groups of goods (finishing materials, elevator equipment, electronics), which provokes an increase in prices with each fluctuation in the exchange rate. Also, the lack of workers forces developers to increase wages, which is directly included in the cost price. It also requires additional capital investments to introduce new requirements for energy efficiency and inclusiveness.

Based on the analysis of the dynamics of recent years and current macroeconomic conditions, it is possible to make a forecast of a further increase in the cost of construction works. It is expected that during 2026 the average annual indicator in Ukraine will increase by another 7–10%, reaching 27.5–28.0 thousand UAH per m2 by the end of the year. In the capital, the cost of construction may cross the threshold of 33 thousand UAH per m2 by the beginning of 2027, taking into account the need to build complex security structures (shelters) in new residential complexes. Also, the difference between the cost of construction in the central and western regions will gradually decrease due to the equalization of prices for logistics and materials. And the start of large-scale infrastructure reconstruction projects may create additional pressure on the market of construction materials, which will provoke another round of cost growth in 2027.