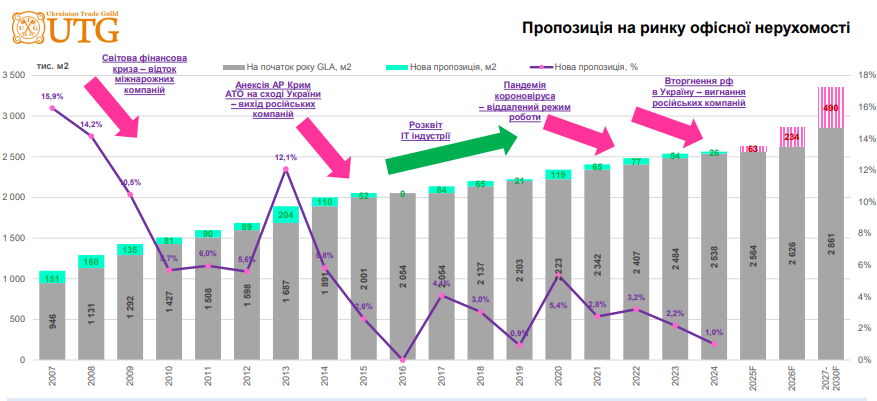

Trends in the Kyiv Office Real Estate Market

Ukrainian office real estate continues to experience difficult times. After 2016-2019, when the development of IT companies provoked a rapid increase in activity and reanimated almost all canned, frozen or postponed projects, in the coronavirus years of 2020-2021 the segment demonstrated a significant slowdown in dynamics: a decrease in the absorption of office space, the transfer of personnel to remote work. But it was the beginning of the military invasion that further intensified the negative trend. The armed aggression of the Russian Federation in 2014 led to the beginning of a mass outflow of Russian companies and their final closure in 2022-2023. Given the massive attacks on the country’s energy infrastructure by the occupiers, unpredictable power outages and the difficulty of attracting new clients reduced administrative and business development activity in this segment to almost zero. Therefore, according to the forecasts of UTG analysts, in the next few years, high volatility of the macroeconomic situation is expected, even with the loyalty and support of the international community to Ukraine and possible accession to the EU and NATO – the number of foreign companies as consumers of office real estate will not allow to quickly absorb all the available supply.

Given the latest global trends in the information technology segment and calls from transnational giant companies for optimization and further reductions, the IT market expects a lull in the coming years. Thus, the Russian Federation’s invasion of Ukraine and the beginning of hostilities, the global coronavirus pandemic and quarantine led to a decrease in the income of most companies while maintaining obligations to counterparties, the payroll fund, tax deductions, etc. Against this background, there is a change in the formats of tenants, a reduction in occupied space, and relocation to areas remote from the center. The largest Ukrainian corporations have transferred employees from rented premises to their own administrative real estate. A number of companies have withdrawn low-demand representative offices, small and medium-sized ones are rationalizing the cost part. The widespread practice of working from home, which began during the coronavirus, continues, which has even deepened due to the threat of mobilization and TRC (territorial recruiting center) employees.

Given the increase in the cost of energy, the increase in utility bills (the need for generators, loss of electricity / working time due to alarms), and with them OPEX – due to the increase in vacancy and the distribution of operating payments to a smaller number of operators, the burden on tenants continues to increase, and rental rates show a further decrease. For example, in February 2025, rent per 1 m2 cost in class “A” = $17.2, in class “B” = $11.7, in class “C” = $9.3 (excluding VAT, OPEX, KP, BOMA). At the same time, the average weighted vacancy rate in business centers in Kyiv at the beginning of 2025 was: in class “A” on average 28.6%, in “B” approximately 21.5% and in class “C” – 14.6%